Small Ways to Make Your Household Budget Easier to Manage

Managing a household budget does not have to mean tracking every penny in a complicated spreadsheet or giving up everything you enjoy. For many people, the best budgeting habits are the small ones. They are the routines that make everyday spending easier to understand, bills easier to plan for, and financial decisions a little less stressful.

Managing a household budget does not have to mean tracking every penny in a complicated spreadsheet or giving up everything you enjoy. For many people, the best budgeting habits are the small ones. They are the routines that make everyday spending easier to understand, bills easier to plan for, and financial decisions a little less stressful.

Whether you are trying to save more, reduce unnecessary spending, or simply feel more organized, a few simple systems can make a big difference. The goal is not perfection. The goal is to create a budget that works with your real life.

Here are practical ways to make your household budget easier to manage.

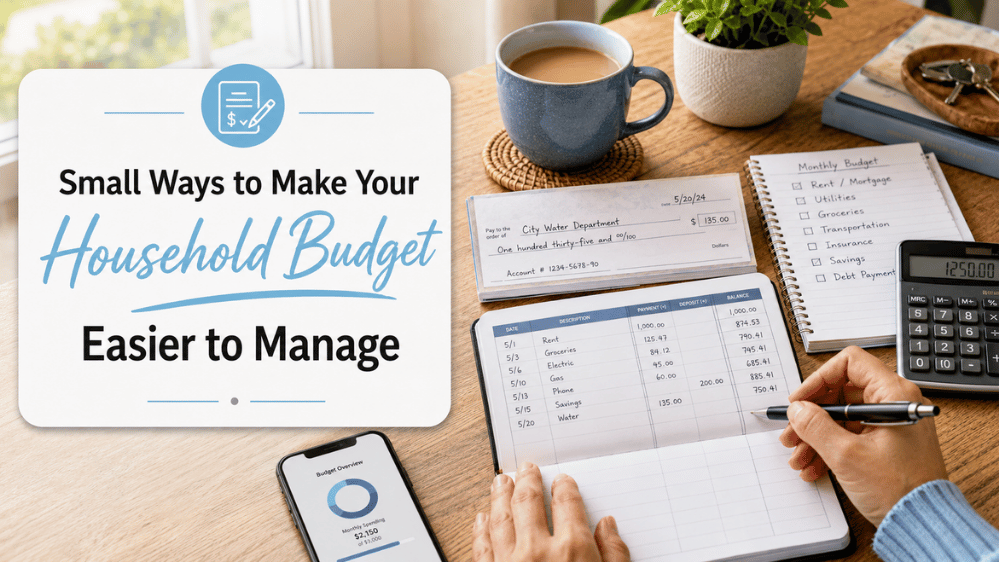

Start With the Bills You Know Are Coming

The easiest place to begin is with the expenses that show up every month. These may include rent or mortgage payments, utilities, phone bills, insurance, subscriptions, internet, car payments, childcare, groceries, and pet expenses.

Instead of starting your budget with what you hope to save, start with what you already know you need to pay. This gives you a clearer picture of how much money is truly available for savings, flexible spending, and unexpected costs.

A simple monthly bill list can help you see:

- What is due

- When it is due

- How much it usually costs

- Which payment method you use

- Whether the amount changes each month

Once you can see your recurring expenses in one place, it becomes easier to spot patterns and make adjustments.

Separate Fixed Costs From Flexible Spending

Not every expense works the same way. Some costs stay fairly consistent, while others change from week to week.

Fixed costs usually include things like rent, mortgage payments, insurance, loan payments, and certain subscriptions. Flexible spending includes groceries, dining out, entertainment, clothing, household items, gifts, and personal purchases.

Separating these categories helps you avoid feeling like your whole budget is out of control. You may not be able to change your rent this month, but you may be able to adjust how much you spend on takeout, impulse buys, or extra shopping trips.

This also helps you make more realistic goals. Instead of saying, “I need to spend less,” you can say, “I want to reduce dining out by $100 this month” or “I want to keep grocery spending under a set amount each week.”

Give Every Payment Method a Purpose

Most households use a mix of payment methods, including debit cards, credit cards, automatic withdrawals, online bill pay, payment apps, cash, and checks. Rather than using whatever is most convenient in the moment, it can help to give each payment method a clear purpose.

For example, you might use:

- A debit card for groceries and everyday purchases

- A credit card for planned expenses you pay off monthly

- Automatic payments for fixed bills

- A checking account for household expenses

- Personal checks for rent, gifts, donations, local services, or payments that need a clear paper trail

This keeps your finances easier to track because you know where certain types of payments are coming from. It can also help prevent forgotten bills, duplicate payments, or confusion when reviewing your bank statement.

Use Checks for Payments You Want to Track Carefully

Even if you do not write checks every day, they can still be useful for specific household expenses. Checks create a record of who you paid, how much you paid, and when the payment cleared. That can be helpful for bills, local services, donations, rent, school expenses, medical payments, or larger household purchases.

Checks can also be useful when you want to avoid card processing fees or when a business, landlord, contractor, or service provider prefers a paper payment.

Keeping checks on hand does not mean you have to use them for everything. It simply gives you another option when a digital payment is not the best fit.

Review Subscriptions Every Few Months

Subscriptions are easy to forget because many of them are small. A few streaming services, apps, memberships, delivery programs, cloud storage plans, and trial offers can quietly add up over time.

Set aside time every few months to review what you are paying for. Ask yourself:

- Do I still use this?

- Is there a cheaper plan?

- Did a free trial turn into a monthly charge?

- Am I paying for two services that do the same thing?

- Would I notice if I canceled this?

Canceling one or two unused subscriptions may not transform your budget overnight, but it can free up money with very little effort.

Plan for Irregular Expenses Before They Happen

Some expenses are not monthly, but they are still predictable. These may include car registration, holiday gifts, school supplies, annual memberships, home maintenance, vet visits, birthdays, travel, tax preparation, or insurance renewals.

Because these expenses do not happen every month, they can feel like surprises when they arrive. One way to make them easier is to create a simple list of expected irregular expenses for the year. Then, divide the estimated cost by the number of months you have to save.

Even setting aside a small amount each month can make these costs feel more manageable when they come up.

Create a “Before You Buy” Pause

Impulse spending is one of the easiest ways for a budget to get off track. That does not mean you can never buy something fun. It just means giving yourself a little space before making a purchase.

For nonessential items, try waiting 24 hours before buying. For larger purchases, wait a few days and compare prices. You may still decide to buy the item, but you will be making the decision more intentionally.

A short pause can help you avoid duplicate items, unnecessary upgrades, or purchases that only felt urgent in the moment.

Keep a Small Buffer in Your Checking Account

A budget can feel stressful when your checking account is always close to zero before the next paycheck. If possible, try to build a small buffer in your checking account so regular expenses do not create constant pressure.

This does not need to happen all at once. You can build it slowly by setting aside a small amount from each paycheck or saving leftover money at the end of the month.

A checking account buffer can help with timing issues, small emergencies, delayed deposits, or bills that clear earlier than expected.

Make Budgeting a Weekly Habit

A monthly budget is helpful, but a weekly check-in can make it easier to stay on track. This does not need to be a long or complicated process. Even 10 minutes can help.

During a weekly budget check-in, you can:

- Review recent purchases

- Check upcoming bills

- Look at your checking account balance

- Plan groceries and household needs

- Make sure automatic payments cleared

- Write or mail any checks that are due

This routine helps you catch small issues before they become bigger problems.

Find Ways to Save Without Feeling Deprived

A budget should help you feel more in control, not like you are constantly being punished. Instead of cutting everything enjoyable, look for small swaps that do not feel painful.

You might cook one more meal at home each week, compare prices before buying household essentials, use what you already have before restocking, borrow items you only need once, or choose a lower-cost version of a routine purchase.

The most sustainable savings habits are usually the ones you can repeat without feeling frustrated.

Keep Your Financial Tools Simple

You do not need the most complicated budgeting system to manage your money well. For some people, a detailed spreadsheet works. For others, a notebook, calendar, banking app, bill checklist, or envelope system is easier.

The best system is the one you will actually use. If your current budgeting method feels overwhelming, simplify it. Focus on knowing what is coming in, what is going out, what bills are due, and what you want to save.

A More Organized Budget Starts With Small Habits

Household budgeting is not about being perfect with money every single day. It is about creating habits that help you make better decisions more often.

When you know your bills, understand your spending patterns, plan for irregular expenses, and use the right payment method for the right situation, your budget becomes easier to manage.

Our mission at Extra Value Checks is to simplify ordering affordable personal and business checks online, so you can keep a practical payment option on hand for bills, household expenses, donations, services, and other payments that still call for a check. With a little planning and the right tools, managing your money can feel less stressful and more organized.